A familiar moment plays out in boardrooms every week. A director asks, “What would a serious data breach cost us?” The CEO looks to the CFO. The CFO looks to the CIO or security lead. Then someone gives an industry average, adds a few qualifiers, and hopes the conversation moves on.

That answer isn't good enough.

If leadership can't explain the cost of a data breach in business terms, the company isn't governing cyber risk. It's budgeting around anxiety. That's how teams end up buying tools without a clear thesis, underfunding the controls that matter, and overexplaining incidents after the fact.

The right question isn't whether breaches are expensive. They are. The right question is simpler and more useful: what would a breach cost this business, in this industry, with these systems, customers, contracts, and obligations? Once you can answer that, security stops being a vague technical concern and becomes what it should be: a financial risk management discipline.

Your Board Asks About a Data Breach What Is Your Answer

The scene is usually the same. A new customer is pushing on security during procurement. An insurer wants sharper answers. The audit or risk committee asks for a clearer view of exposure. Leadership asks for a number, and what they get is a blend of benchmark data, instinct, and wishful thinking.

That gap is a governance failure, not a technical one.

Boards don't need packet captures or firewall settings. They need a defensible explanation of exposure, decision rights, and readiness. If management can't say which data matters most, what a serious incident would interrupt, and what the first month of response would likely cost, then the business is carrying material risk without a working model for it.

Why the usual answer falls apart

Most executive teams have one of three weak responses:

- They quote a market average and assume it applies to them.

- They point to cyber insurance as if transfer is the same as control.

- They talk about tools instead of impact, timelines, and obligations.

None of those answers helps a board allocate capital or exercise oversight.

Board standard: If your breach answer would change dramatically depending on who is in the room, you don't have a risk model. You have talking points.

A better answer starts with a simple admission. Your exact loss number won't be perfect. It doesn't need to be. It needs to be reasoned, documented, and good enough to support decisions about investment, reporting, and preparedness.

That's also why board reporting needs to mature beyond vague heat maps and status updates. If you need a stronger structure for that discussion, this board-ready cybersecurity reporting template is a useful starting point.

What leadership should be able to say

By the time this question reaches the board, management should already be able to answer:

- What would hurt most: Which systems, records, or business processes create the largest financial exposure.

- What the first-order costs are: Legal, forensic, notification, regulatory, and recovery work.

- What the second-order costs are: Revenue disruption, customer loss, contract issues, and leadership distraction.

- What reduces the loss fastest: The controls and response capabilities that shorten the incident timeline.

If you can't answer those four points clearly, don't ask for a bigger security budget yet. Build the exposure model first.

Beyond the Headline The Full Cost Profile of a Breach

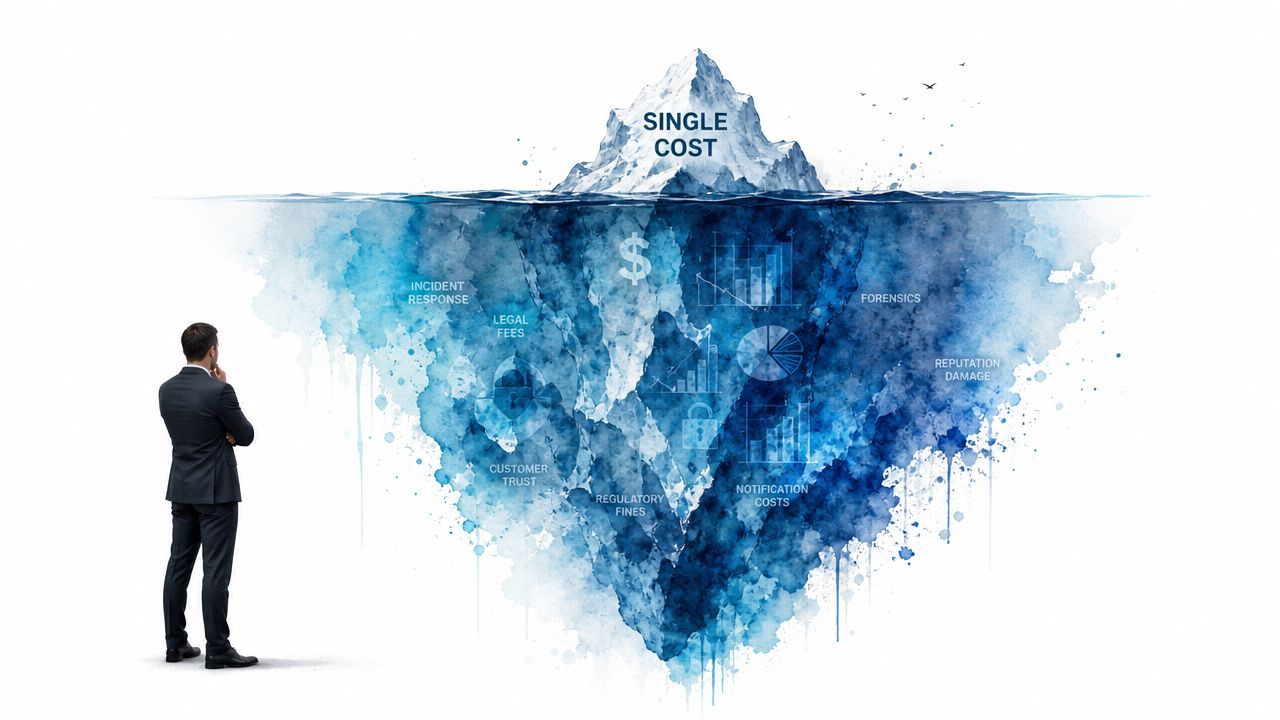

Most discussions about the cost of a data breach are too shallow. They collapse a messy business event into one headline number and move on. That's convenient, but it hides where the real damage shows up.

IBM reported that the global average cost of a data breach was $4.44 million in 2025, down 9% from the prior year, and tied that decline to faster identification and containment. The same report put the U.S. average at $10.22 million, nearly 2.3 times the global average, and found that 13% of organizations experienced a breach related to AI (IBM Cost of a Data Breach Report 2025).

Those figures are useful for context. They are not a budget.

The visible costs above the waterline

These are the costs leadership usually expects because they show up quickly and arrive with invoices.

- Forensic investigation: External specialists determine what happened, what was touched, and whether the attacker still has access.

- Legal and regulatory response: Counsel, privilege management, disclosure analysis, and interaction with regulators.

- Notification and remediation: Customer notices, call center support, identity-related services where appropriate, and urgent control fixes.

- Technical recovery: Rebuilding systems, restoring access, validating data integrity, and hardening the environment.

Finance teams can usually estimate these categories with some discipline. They are painful, but they are legible.

The larger mass below the waterline

The harder costs to manage are the ones that don't arrive as a single bill.

A breach can interrupt order flow, delay service delivery, freeze change activity, and pull senior operators into daily crisis management. Sales teams lose momentum because prospects ask harder questions. Existing customers slow renewals or demand concessions. Internal projects stop while IT, legal, finance, operations, and communications all shift into incident mode.

That's why many breach discussions understate the actual business impact. The accounting view catches the direct spend. The operating view catches the drag.

A breach is rarely just a security event. It becomes a finance event, a legal event, a customer event, and an execution event at the same time.

What boards should focus on instead

Don't ask only, “What's the total cost?” Ask how the cost breaks down:

| Cost layer | What it usually includes | Why leadership should care |

|---|---|---|

| Direct response | Forensics, legal, outside advisors, emergency technical work | Immediate cash outlay and board scrutiny |

| Regulatory and contractual | Notification obligations, customer commitments, sector requirements | Can reshape deal risk and oversight burden |

| Operational disruption | Downtime, delayed projects, manual workarounds | Slows revenue and weakens execution |

| Commercial fallout | Customer trust issues, churn risk, pricing pressure | Hits growth and margin after the incident |

Once you see the full profile, the leadership task gets clearer. You're not only trying to avoid a fine. You're trying to reduce interruption, compress decision time, and protect trust.

Why Industry Averages Are Dangerously Misleading

A global average is a rough weather report. It doesn't tell you what happens on your street.

Industry matters because the cost of a data breach is shaped by the type of data involved, the response obligations that follow, and the scrutiny that lands after disclosure. IBM data covering the March 2022 to February 2024 period showed healthcare at $9.77 million, financial services at $6.08 million, and the public sector at $2.55 million on average (industry breach cost comparison from Statista citing IBM data).

That spread should change how boards think. It shows that breach economics are not driven only by incident size. They are driven by consequence.

Why healthcare gets punished harder

Healthcare sits in the expensive end of the range for obvious reasons. The data is particularly sensitive. The notification burden is demanding. The downstream work often involves legal review, forensics, patient communication, operational workarounds, and intense reputational exposure.

A provider or healthcare services organization also has a brutal business reality: incident response can disrupt care operations, scheduling, claims workflows, vendor access, and staff productivity at the same time. That's not just a privacy problem. It's a continuity problem.

Financial services carries a different kind of exposure

Financial organizations deal with another hard mix: regulated environments, consumer trust sensitivity, and quick reputational fallout when controls look weak. Customers don't tolerate uncertainty well when money movement, account access, or fraud risk are involved.

That means a financial breach can become expensive not only because of formal response requirements, but because confidence erodes fast and every remediation step is closely watched by customers, counterparties, auditors, and regulators.

Practical rule: If your industry has sensitive data and visible oversight, assume your breach cost profile will be pushed upward by response complexity, not just by the number of records involved.

What leaders should do with this

Don't budget off a generic average. Build around your sector and your obligations.

Start with three filters:

- Data sensitivity: Would exposure involve health, financial, legal, employee, or other high-trust information?

- Regulatory burden: What disclosures, investigations, and response steps would your sector trigger?

- Operational fragility: Which core workflows would slow or stop during containment and recovery?

Leaders often ask for one benchmark number because it feels tidy. But tidy is not the same as useful. A public-sector style cost assumption inside a healthcare or financial environment is not conservative. It's careless.

A Practical Model to Calculate Your Financial Exposure

You don't need a massive quantitative risk program to get useful answers. You need a working estimate that finance, operations, legal, and technology leaders can defend in the same room.

Start by framing one event. Not every possible cyber scenario. One serious breach that hits a meaningful part of the business.

Pick the breach that would actually matter

Don't begin with abstract threat lists. Begin with your crown jewels.

That might be your customer records, claims platform, payment environment, donor database, product data, HR files, or the system that keeps revenue moving. If the wrong asset gets exposed or unavailable, the loss won't come from one line item. It will ripple through multiple functions.

A useful working model asks:

- Which data or system would create the largest business interruption if compromised?

- Which obligations would trigger first?

- Which customers, partners, or regulators would need answers immediately?

- Which leaders would have to stop normal work to manage the incident?

Build the estimate in layers

In this situation, executives often overcomplicate the exercise. Don't. Use ranges.

Think in low and high estimates for each category. The low estimate assumes a contained incident with a disciplined response. The high estimate assumes the incident is broader, slower, and more disruptive.

| Cost Component | Factors to Consider | Low Estimate ($) | High Estimate ($) |

|---|---|---|---|

| Legal and regulatory response | Outside counsel, notification analysis, sector-specific obligations | ||

| Forensics and technical containment | External investigators, emergency support, system review, cleanup | ||

| Operational disruption | Downtime, delayed transactions, missed work, overtime, manual fallback | ||

| Customer and commercial impact | Contract issues, concessions, delayed deals, lost renewals | ||

| Recovery and hardening | Rebuild work, security improvements, vendor support, extra monitoring |

This is intentionally simple. It forces the right conversation.

A worked example without fake precision

Take a hypothetical mid-sized services company. It stores regulated customer information, runs on a handful of key SaaS platforms, and depends on uninterrupted client access to deliver work. A breach exposes sensitive records and forces the company to suspend some operations while it investigates and contains the incident.

The finance lead estimates the direct response costs. The operations lead estimates what a week of disruption would do to delivery and backlog. Sales and customer success estimate likely concessions, delayed starts, and renewal pressure. Legal maps out the response obligations. Technology estimates the cost of containment, recovery, and urgent hardening.

Now leadership has a range, not a guess.

If your estimate feels uncomfortable, that's usually a sign the exercise is working. Exposure should be clarifying, not soothing.

Make the number useful

The point of this estimate is not actuarial perfection. The point is to support choices:

- Budget choices: Which controls deserve funding first.

- Insurance choices: Whether coverage, exclusions, and limits align with likely loss areas.

- Vendor choices: Which third parties create concentrated risk.

- Board reporting choices: Which metrics belong in front of the risk committee.

- Preparedness choices: Where testing and tabletop work will reduce confusion during an incident.

If you want a companion read that frames cyber exposure in financial language for operating leaders, this CEO's guide to cyber risk assessment in financial terms for mid-market growth is worth reviewing.

What usually goes wrong

Three mistakes show up again and again:

- Using one blended number: That hides where the loss really comes from.

- Ignoring operating drag: The business interruption piece is often undercounted.

- Leaving out decision-makers: If finance, legal, operations, and commercial leaders don't contribute, the estimate won't survive scrutiny.

A rough but cross-functional estimate beats a polished security-only estimate every time.

The Biggest Cost Drivers and How to Control Them

The breach itself matters. The timeline matters more.

IBM's 2025 findings, summarized by Baker Donelson, reported a global average breach cost of $4.44 million and tied the decline from the prior year to faster identification and containment. The same summary noted the U.S. average reached $10.22 million, with higher regulatory fines and detection-and-escalation costs helping drive that record level (Baker Donelson summary of IBM's 2025 breach cost report).

That tells leaders where to focus. Not on security theater. On speed, clarity, and execution under pressure.

Detection speed is a business control

When attackers stay in your environment longer, the event gets more expensive in predictable ways. More systems may be affected. More data may be touched. More uncertainty surrounds disclosure. More executives get pulled in. More outside support is needed.

That's why boards should care about detection and containment capability. It is not just an IT metric. It is a cost control.

A mature team knows how it will detect unusual behavior, who will triage it, who can authorize urgent containment, and which outside parties are already on call. An immature team burns days deciding who owns what.

Incident response readiness changes the bill

A documented incident response plan isn't enough. It has to be tested.

If legal, communications, operations, technology, and executive leadership haven't rehearsed together, the first real incident becomes the rehearsal. That is expensive. People duplicate work, hold approvals too long, notify too early or too late, and create confusion that slows containment.

The strongest cost levers are often mundane:

- Clear roles: Who declares the incident, who leads it, who approves major actions.

- Retained specialists: Counsel, forensics, and communications support lined up in advance.

- Tabletop exercises: Leaders practice decisions before they have to make them under pressure.

- Priority restoration plans: The business knows what must come back first.

A breach rarely becomes catastrophic because one control failed. It becomes catastrophic because the organization responded slowly, vaguely, and with unclear authority.

Spend where cost compression is real

If budget is limited, don't spread it evenly to make everyone feel included. Put it where it shortens the timeline and improves decision quality.

That often means investing in:

- Better visibility across identity, endpoints, cloud systems, and high-value data paths.

- Faster triage and escalation so suspicious activity reaches accountable people quickly.

- Practical incident planning with named owners and tested communications.

- Focused hardening around the systems and data that would create the largest loss.

That's also why prevention and response shouldn't be treated as separate conversations. If you want a practical operating view, this guide on how to prevent data breaches is a useful complement to the cost discussion.

An Executive Checklist for Reducing Breach Costs

Most executives don't need more cyber jargon. They need sharper questions.

Healthcare remains one of the most expensive sectors for breaches, with average costs reported in a range from $7.42 million to $9.77 million depending on the IBM year cited, reflecting the heavier burden of regulatory response, notification, forensic work, and business interruption compared with lower-cost sectors (CMIT Solutions summary of industry breach cost patterns).

That's the reminder. Your sector changes the exposure. Your governance determines whether the response is controlled or chaotic.

Questions to put on the table now

Use these in your next leadership meeting or risk committee session.

- Do we know our highest-cost breach scenario: Not the most cinematic scenario. The one most likely to produce serious business loss.

- Can finance, legal, operations, and technology defend the same exposure estimate: If each function gives a different answer, the model isn't ready.

- Which systems and data create the largest interruption risk: If those assets aren't named, protected, and monitored differently, priorities are off.

- Who has authority during the first day of an incident: Delayed decisions are expensive decisions.

- Have we tested our incident response with actual executives in the room: A plan that hasn't been exercised is paperwork.

- Do our major vendors increase our exposure in ways we haven't priced in: Outsourced risk is still your risk.

- Would our insurance respond the way leadership assumes it will: Assumptions around coverage often collapse under exclusions and process requirements.

What good answers sound like

Good answers are specific, cross-functional, and boring. That's a compliment.

They identify the critical systems, the likely obligations, the response owners, the outside partners, and the financial range leadership is using for planning. They also make clear what the company is doing to reduce the likely loss, not just the likelihood of an event.

Boards should ask for evidence of readiness, not reassurance. Reassurance is cheap. Readiness takes work.

What weak answers usually reveal

Weak answers usually point to one of four issues:

| Warning sign | What it usually means |

|---|---|

| “We're aligned with industry averages” | No company-specific exposure model |

| “Our MSP handles that” | Ownership is fuzzy |

| “We have a plan somewhere” | Response hasn't been operationalized |

| “Insurance should cover most of it” | Leadership may be overestimating transfer and underestimating exclusions |

The point of this checklist isn't to create fear. It's to force clarity.

From Guesswork to Governance

A company doesn't become safer because it talks more about cyber risk. It becomes safer when leadership can explain exposure clearly, assign ownership cleanly, and fund the few actions that reduce loss meaningfully.

That is the shift. Move from generic averages to a company-specific estimate. Move from technical activity to financial consequence. Move from hoping the team can improvise under pressure to knowing who will do what, when, and with what authority.

This is also where cyber risk belongs alongside other insurable and operational exposures. Leaders who are already tightening their broader risk posture may also find Professional Insurance Advisors on managing accounting risk useful, because the same discipline applies across domains: identify the concentrated exposure, define controls, and don't confuse paperwork with protection.

You will never eliminate breach risk. That isn't a serious objective.

You can, however, make it governable. You can estimate the financial downside with enough rigor to make better budget decisions. You can identify the highest-cost scenarios. You can tighten the response path so the incident doesn't sprawl into a wider business failure. And you can give your board a better answer than “it depends.”

That's the standard now. Not perfection. Clarity.

If technology risk feels hard to explain, hard to govern, or too dependent on guesswork, CTO Input can help you make it legible. A Clarity Call is a practical next step to surface your biggest exposure areas, tighten ownership, and outline the first moves to reduce breach cost and improve board confidence.